And before college football kicks off in less than two weeks, we think it could be beneficial to update y’all on where we currently stand regarding a recession.

By reflecting back on our 15 Reasons for a Recessionpost — we can use this as a “heat check” on the progress that’s been made.

While we’re still very wary of the total debt balance, consumer credit, an inverted yield curve, and much more — there have been some improvements to important things like inflation, gas prices, and the supply chain.

The chart below from Charlie Bilello shows that global container freight rates have hit a 15-month low, down -46% from their peak:

However, keep in mind that this price is still 4x higher than pre-pandemic levels and the vast majority of the ‘15 Reasons’ still remain problematic (rising interest rates, inflation, layoffs, etc).

Unfortunately, even if inflation really did peak in June — the Consumer Price Index (CPI) wouldn’t reach the Fed’s 2% target any time soon. We’re not saying that you should sit on the sidelines, but it’s critical to remind you that this is likely to remain a stock-picker’s market and there’s probably going to be broader downside after this bear market rally concludes.

A massive update on this bear market rally as well as the markets in general is coming out tomorrow (8/16) afternoon. Read it!

The Investing Week Ahead — Too Long, Didn’t Read:

⚡ Walmart, Target, & Home Depot lead the way for a retail-filled earnings week.

⚡ Hedge funds reveal their cards.

⚡ Housing and jobs are top of mind as the FOMC meeting minutes get released.

Key Earnings Announcements:

Big box retailers face the fire after most of them have downwardly revised guidance throughout the summer.

Monday (8/15): Clear Secure, Compass, Tencent Music Entertainment, Weber, ZipRecruiter

Tuesday (8/16): Agilent Technologies, Home Depot, ON Holding AG, Sea Limited

Wednesday (8/17): Analog Devices, Bath & Body Works, Cisco, Krispy Kreme, Lowe’s, Synopsis, Target, TJ Maxx,

Thursday (8/18): Applied Materials, Bill.com, BJ’s, Estēe Lauder, Kohl’s, Ross

Friday (8/19): Foot Locker, John Deere

What We’re Watching:

Retail First, Last, and Always: “Big box” earnings reports are sure to be the bellwether of the week. This summer, both Walmart (July / August) and Target (June) slashed their forward guidance and forecasted some logistical turbulence ahead. JPMorgan recently noted that Walmart may be in a position to benefit from a consumer trade-down effect as shoppers seek cheaper deals. Analysts are less bullish on Target, as it’s considered to carry a much higher percentage of discretionary products. Either way, back-to-school shopping is expected to give both stocks a healthy revenue injection.

Safe Travels: Clear Secure (YOU 4.84%↑) is a stock in the ‘Moonshot’ category of my portfolio that has remained in the green throughout these turbulent times. At the time of writing this, the company has just released their results this morning. Revenue of $103M was up +86% and Total Bookings of $123M was up +75%. The most impressive takeaway is that Total Cumulative Enrollments of 13M was up +107%. We’ve seen many friends enrolling in the service, despite it only being offered at 45 airports thus far. Given the apparent comeback of Americans traveling (regardless of market conditions) — this play has the feeling a true, long-term hold. Below is a graph I pulled from their shareholder letter.

Investor Events:

Michael Burry goes all-in on one stock with a market cap under $1B, single stock ETFs fool investors, and FuboTV has a shot at being acquired.

Hedge Fund 13F Filings: Today is the last day for hedge funds to report their holdings. We’ll report in the next Week in Review on a variety of major players to see what they’re buying and selling. Keep in mind that these are for the trailing quarter and many of the position changes can be 30-45 days delayed.

Also… check out what Michael Burry did. We spoke about his concerns in yesterday’s post — now he has sold everything and gone all in on a company that invests in private prisons and mental health facilities. Wow. We’ll definitely look deeper into this and keep an eye out for a video being posted on it.

Single-Stock ETFs? What..?: If you weren’t aware, Wall Street has been pouring gasoline on the latest financial craze for trying to receive outsized returns. Throughout 2022, single-stock ETFs have grown exponentially in popularity — as they allow you to get short or leveraged exposure to the daily price moves of the underlying stocks. Some examples include the GraniteShares 1.25x Long TSLA Daily ETF (TSL), GraniteShares 1x Short TSLA Daily ETF (TSLI), GraniteShares 1.75x Long AAPL Daily ETF (AAPB), and the GraniteShares 1.5x Long COIN Daily ETF (CONL). AXS Investments has launched / soon will launch single-stock ETFs of Boeing (BA), Salesforce (CRM), PayPal (PYPL), Microsoft (MSFT), Netflix (NFLX), and more. Please do not invest in these financial instruments unless you know what you’re doing. They focus purely on daily price moves and are nothing short of gambling.

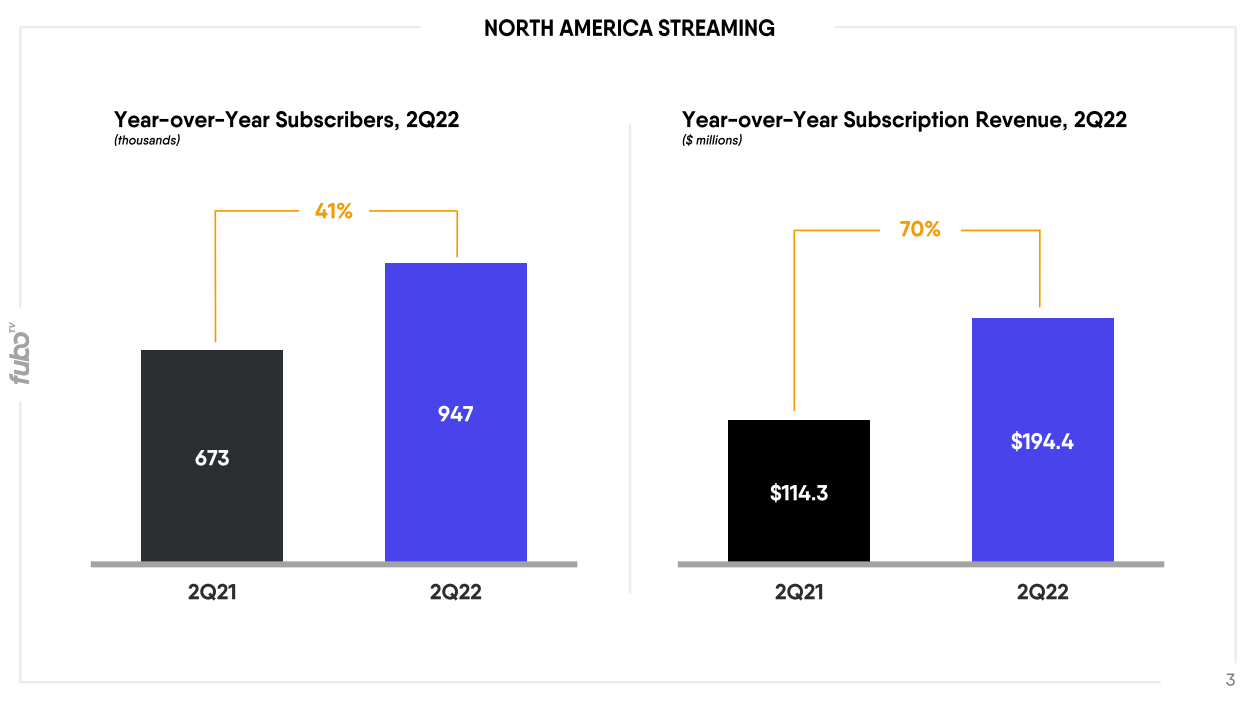

FuboTV’s First-Ever Investor Day: There’s been rumors that FuboTV could be an acquisition target from MGM Resort’s BetMGM or FanDuel. Below shows the impressive growth of the streaming service:

FuboTV (FUBO) Q2 Earnings Presentation

Major Economic Updates:

The Fed has rocked the housing market, but the results continue to be less than ideal.

Tuesday (8/16): Building Permits, Housing Starts, Industrial Production Index

Wednesday (8/17): Business Inventories, Retail Sales, July Meeting Minutes from the Federal Reserve

Thursday (8/18): Existing Home Sales, Jobless Claims

All Week: Fed Presidents Speak (Waller, Bowman, George, Kashkari, Barkin)

What We’re Watching:

Home Builder’s Index (Today)

The NAHB Housing Market Index extended declines for an eighth consecutive month to 49 in August of 2022 — the lowest reading since May of 2020 and well below market forecasts of 55. Anything above 50 is considered positive. The index has not been in negative territory since a brief plunge when the pandemic began. Before that, it hadn’t been negative since June 2014. The difficult consideration here is that the Fed wants to lessen overall demand, as well as make housing more affordable. Demand has surely been impacted, but housing prices still remain dramatically high.

National Association of Home Builders Housing Market Index

“Tighter monetary policy from the Federal Reserve and persistently elevated construction costs have brought on a housing recession. The total volume of single-family starts will post a decline in 2022, the first such decrease since 2011. However, as signs grow that the rate of inflation is near peaking, long-term interest rates have stabilized, which will provide some stability for the demand-side of the market in the coming months” — NAHB Chief Economist Robert Dietz.

Retail Sales (Wednesday)

As consumer credit has soared in America, retail sales have been relatively unpredictable. Results have come in all over the place over the last year, rarely matching expectations. Analysts expect a measly +0.1% increase for July.

Retail Sales, Month-over-Month percent change

Jobless Claims (Thursday)

Unlike most economic data, jobless claims are reported each week. While we typically ignore them and focus on monthly jobs reports, we’re just flagging that it may be time to start paying closer attention. The labor market has been strong, and any signs of weakness the rest of the year could be poorly received by the broader market.

Jobless Claims by Month, in Thousands

Events-Driven Winners

Companies continue to pile on the buybacks — likely because the Inflation Reduction Act passing would create a new tax on doing so in the future.

Our friends at LevelFields scrub through thousands of data points each week to determine how events impact stock prices.

It’s painful to see in real time — but shareholders often love to see layoffs. Employee headcount is always among companies’ largest expense categories, especially after hiring like crazy during a bull market. Atara Biotherapeutics & Peloton joined the ranks below of companies that slashed headcount last week:

Peloton — 13%

Best Buy — “hundreds”

Calm — 20%

Truepill — 33%

Wix — 100 employees

Hootsuite — 30%

Sweetgreen — 5%

Linktree — 17%

Vroom — 337 employees

iRobot — 10%

(percent of total workforce)

If you’re starting your investing journey or want to change to a cleaner, social-focused investing platform, consider visiting Public.com.

Disclaimer: This is not financial advice or recommendation for any investment. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.