And it’s shaping up to be quite a weird month. As we extensively broke down in yesterday’s Week in Review, the stock market appears to be looking past still-aggressive Fed rate increases and two consecutive quarters of GDP contraction — which is what has always been defined as being a recession.

No political agenda here — the above graphic is just a great one.

On one hand, the central government and some media outlets are being completely delusional about how bad some things still are (consumer sentiment, savings balances, inflation, etc).

On the other hand, there’s some reason for positivity. We must not forget that the lion’s share of the major US ETFs & indices are comprised of mega-companies like Amazon, Apple, Alphabet, etc. While the short-term profitability of the largest companies in the S&P has taken a hit, investors appreciated their strong earnings beats.

We wanted to share again a quote that was included in yesterday’s Week in Review:

“The biggest takeaway for me on events of this week? Convincing and arguably decisive evidence the ‘bottom is in’ — the 2022 bear market is over.” — Tom Lee, Managing Partner & Head of Research at Fundstrat

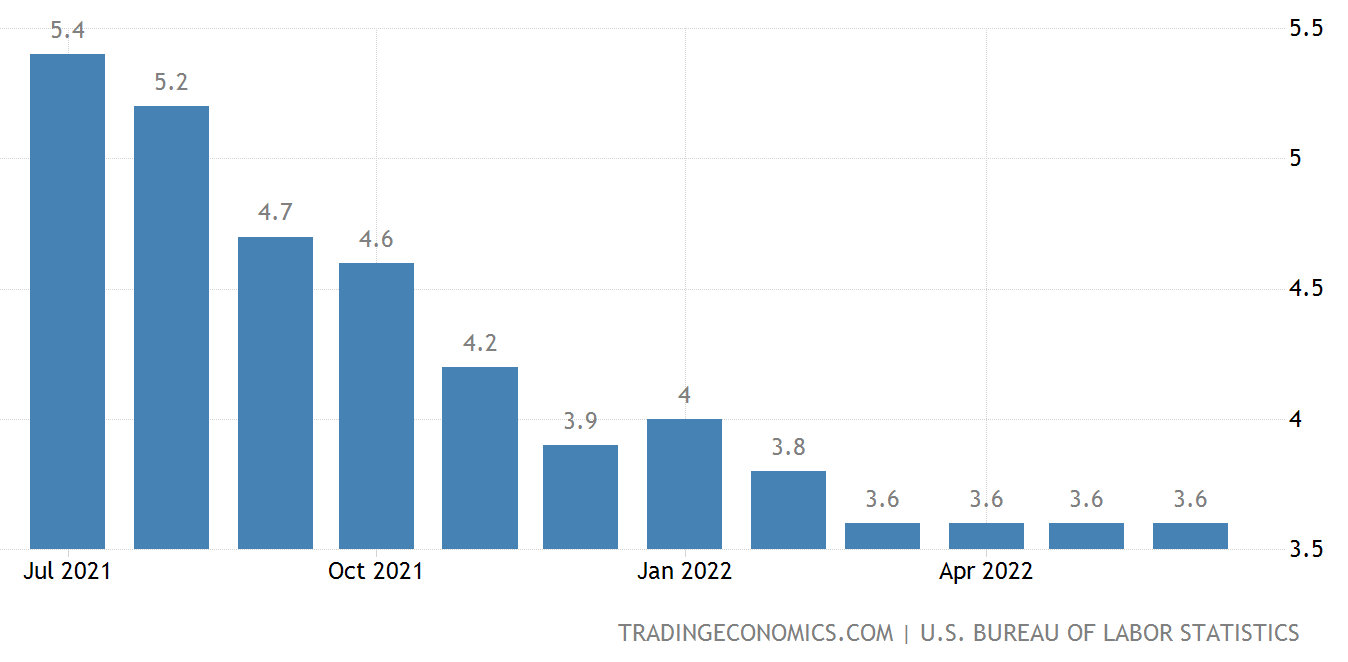

That’s all fun and good, but then you look below for the reality of inflation’s runaway status — especially when compared to the Fed’s target of 2% annualized inflation. We don’t believe we can get anywhere close to it without substantially more Fed interest rate hikes.

We don’t see how 1) inflation continuing to remain so high (even if it’s peaked) and 2) the Fed continuing to raise rates aggressively (even if it’s not higher than 75 bps per meeting) could add up to a bottom already being in. Remember — the stock market is forward looking, but that doesn’t mean it’s clairvoyant on further earnings compression.

We could be wrong, but we’d be surprised to not see the S&P 500 (SPY 0.50%↑) head back down toward the lower 3000s at some point in the coming 6-12 months. As always, if you’re here for the classic what do I do? answer— odds are that your best bet is to DCAon a relatively regular schedule and keep going hard at work. This market is unpredictable.

The Investing Week Ahead — Too Long, Didn’t Read:

⚡ Airbnb, AMD, Cloudflare, PayPal, Starbucks, Twilio, Uber, & many more headline another massive week of earnings reports.

⚡ International updates: Chinese EV deliveries, UK rate hikes, & oil output.

⚡ Household debt & consumer credit provide a serious gauge of recession severity.

Key Earnings Announcements:

Another full week of reports will impact if the market remains trending up and to the right.

Thursday (8/4): Alibaba, AMC, Block, Carvana, Cloudflare, ConocoPhillips, Crocs, Datadog, FuboTV, Kellogg’s, Paramount, Penn National Gaming, Twilio

Friday (8/5): Canopy Growth, DraftKings, GoodYear, Western Digital

What We’re Watching:

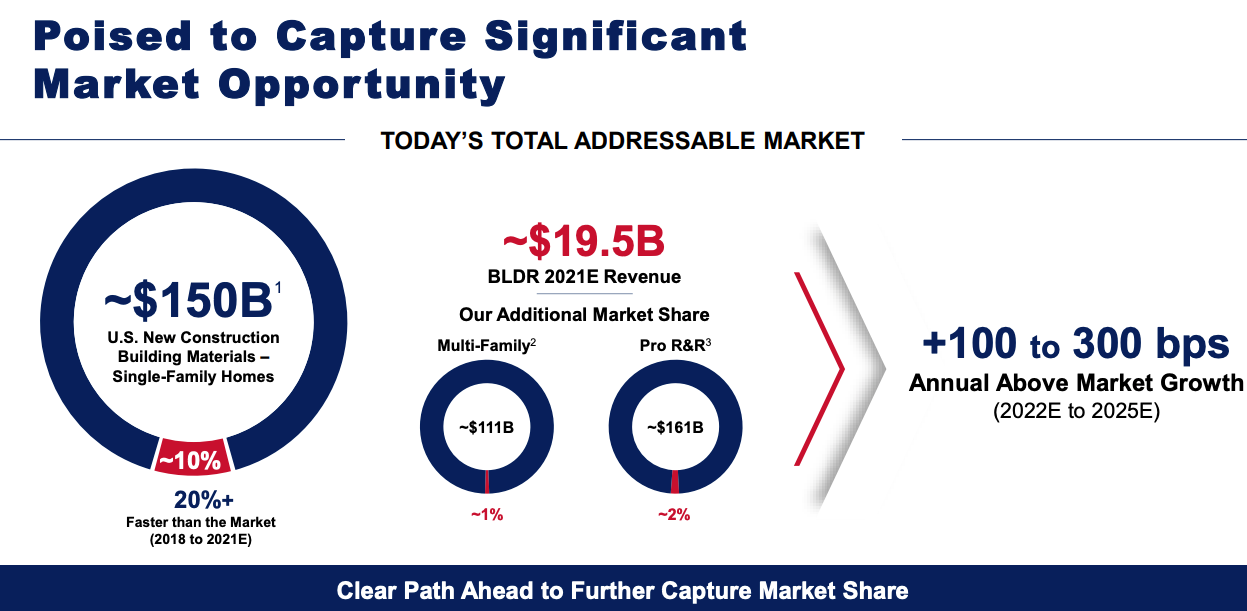

Bob the Builder Would Be Proud: As many of you know, BLDR -0.26%↓ makes up ~7% of my overall portfolio. The company reported earnings this morning and smashed through Wall Street’s expectations. With core organic growth and the acquisition of hardware supplier HomCo, we’ll be watching for more analysts’ reviews of Builders FirstSource. Being up +4% over the last six months isn’t beating inflation, but it sure is better than most.

Builders FirstSource (BLDR) 2021 Investor Day

Uber-Confused: To be transparent, this is one of the most difficult stocks to properly value. On one hand, high-level growth is phenomenal. Gross Bookings of $26.4B were up +35% YoY last quarter. Revenue grew +136% YoY to $6.9B. Adjusted EBITDA of $168M was up +$527M YoY. But the negatives are just too freaky. This company has still never been consistently profitable and makes wacky decisions like striving for nationwide shipping. In order to achieve profitability across the board, it seems that their subscription service (below) would need to gain more traction for improved cash flow projections. Nonetheless, Amazon decided to partner with their food delivery competitor, GrubHub. Mix this in with Lyft (LYFT 2.05%↑) being a worthy competitor and newcomers like Blacklane trying to take their business Uber Black business — we just can’t get ourselves to want exposure to this stock.

Hey Dude!: If you want to kick yourself for something, it should be not listening to our friend Chris Camillo’s calls for Crocs (CROX 2.04%↑) to be an absolute ripper (we didn’t either). The company acquired men’s comfort shoes ‘Hey Dude’ and they have been Amazon best-sellers for months. This has been a crazy story and their earnings report on Thursday will determine if it gets any crazier.

We take things ~international~ for this week’s important events.

Wall Street & Seeking Alpha Ratings of Top EV Stocks

Chinese EV Deliveries came out this morning for Li Auto (LI 1.69%↑), Nio (NIO -0.35%↓), and XPeng (XPEV -1.29%↓). Car deliveries jumped in July, with jumps of +21.3%, +26.7%, and +40% YoY, respectively. Meanwhile, Tesla (TSLA -1.26%↓) soared this morning on the news of a new battery materials deal in China. It’s critical to pay close attention to Elon Musk, as he often has began selling shares of his own stock after months of 30%+ price appreciation. Tesla also makes up over 2% of SPY 0.50%↑, explaining why the S&P 500 recovered slightly after an initial, market-open plunge.

The Bank of England is widely expected to raise rates by +0.5% — which would be the largest hike since 1995. Only three BoE officials voted in favor of a +0.5% rate hike at the bank’s last two meetings, but data since then has shown inflation hitting a four-decade high of 9.4%. It could hit 12% by October — six times the BoE target (Investing.com).

Begging for Increased Oil Distribution continues as the OPEC+ group decides this week whether oil production targets are held at current levels or increased. The most recent reporting suggests that there’s not much support for an increase. If you haven’t noticed, world leaders that were previously reliant on Russian oil imports have been kissing the feet of oil leaders like Saudi Arabia’s Crown Prince or the highest ranking members of North African governments. For some perspective — Russian natural gas accounted for 40% of EU demand in 2021. Keep an eye on these 10 oil companies this week for a reaction, as well as Warren Buffett’s beloved Occidental Petroleum (OXY 0.00).

Tension Warning:

While we’re on the topic of international risk, be sure to pay close attention to what’s going on with China and Taiwan. First off, sources have said that a senior official in Beijing said that Biden’s recent meeting with President Xi exemplified the toughest attitude that the Chinese leader has shown toward any world leader. Mix this in with Nancy Pelosi visiting Taiwan despite Chinese warnings not toand rumors that China has moved military tanks to its region closest to Taiwan — and you’ve got a situation that could get ugly.

Major Economic Updates:

All investors are eyeing July’s jobs report — specifically to see if the unemployment rate begins to tick upward.

Monday (8/1): Construction Spending, ISM Manufacturing Index

Tuesday (8/2): Homeowner & Rental Vacancy Rate, Job Openings & Quits, Real Household Debt, Speech by St. Louis Fed President

Wednesday (8/3): Factory Orders, ISM Services Index

Thursday (8/4): Speech by Cleveland Fed President, Trade Deficit

Friday (8/5): Consumer Credit, July Jobs Report

What We’re Watching (Beyond Unemployment):

Household Debt vs. Savings: Popular investor Bill Ackman recently made claims that while the personal savings rate of Americans has dropped dramatically — it is still in plenty healthy of a condition. “Even if the savings rate were to reach and stay at 0%, it would take ~2 years for consumers to fully deplete the ~$2.6 trillion in excess savings.” His team believes that excess savings are concentrated in households within the top 20% of income distribution, which also account for 40% of all spending. In other words, he believes richer Americans can keep the economy afloat — even if personal savings are zero for the majority of us. Interesting to see comparisons to pre-Great Financial Crisis savings levels. Household debt figures this week should paint a better picture of current pain points for American families.

Swiping Way Too Much: As a bit of a counterargument to Ackman above, we’re not so sure that he’s properly accounting for the massive amount of credit that Americans are taking on. It seems a bit naive to say that personal savings are about the same that they were pre-2008, when consumer loans have compounded significantly. Bad debt and increased loan defaults would undoubtedly rock the system, regardless of if the richest Americans have ample savings in the bank. We’ll be paying close attention to the consumer credit report on Friday.

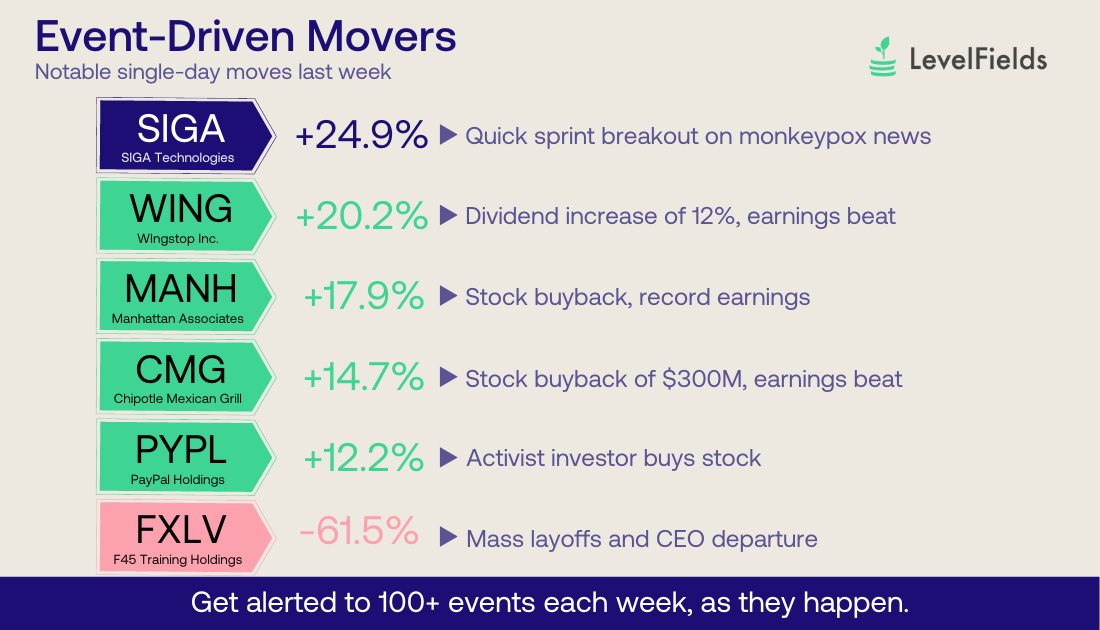

Events Driven Winners:

What specific events are moving stocks the most?

Our friends at LevelFields scrub through thousands of data points each week to determine how events impact stock prices.

Hot damn! We had heard stories of some people that bought into SIGA Technologies (SIGA -7.13%↓) years ago because a smallpox-like outbreak was “bound to happen again.” Boy do we wish we had listened, as the company has soared given monkeypox treatments now being needed around the world. Shoutout to LevelFields for bringing this stock back to the forefront.

If you’re starting your investing journey or want to change to a cleaner, social-focused investing platform, consider visiting Public.com.

Disclaimer: This is not financial advice or recommendation for any investment. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.