Aritzia: the Next Lululemon?

A deep dive analysis on Aritzia and how they’re positioning themselves to take the United States by storm.

Aritzia — a design house offering “Everyday Luxury”

We believe in high quality, beautifully designed product.

We believe in aspirational environments and experiences.

We believe in personalized and engaging client services.

And we believe that all of this should be attainable.

In this post, we’ll cover:

-

A quick rewind on when I shared this stock with you all ~4 weeks ago

-

An introduction to the company & how they navigated COVID

-

My thoughts about the company’s recent earnings call

-

Their main growth drivers as we look into the future

Let’s Rewind

About 3 weeks ago, I shared the below post with you all. It was to give you a heads-up of a major social arbitrage callout my friends at Dumb Money identified — Aritzia.

My Favorite Stocks + Portfolio Update: 1/12/22

If you’re not familiar, Chris, Dave, and Jordan of Dumb Money are hawks as it relates to identifying social trends that could impact stock prices. And there’s no hiding the 600M views on countless videos that contain the word “Aritzia” within their captions on TikTok — almost all of which garnered their views after August 2021.

Here’s the 17-minute long video the three of them published to YouTube the week before the company’s earnings results were shared.

Turns out they were entirely correct — Aritzia published stellar earnings:

*All amounts in Canadian dollars ($1 CAD = $0.79 USD)

-

Revenue: $453.3 million, an increase of +63% YoY

-

Gross Profit: $210.1 million, an increase of +67% YoY

-

Operating Income: $91.0 million, an increase of +89% YoY

-

Profits: $64.9 million, an increase of +113% YoY

Look at those % increases again. I now have your attention.

That’s right, this Canadian clothing company grew revenue by over +60%, operating income by nearly +90%, and profits by more than +110% year-over-year. As you can imagine, their stock is trading much higher since reporting these results.

However, I believe that their stock price will continue to appreciate over the coming 2-4 years. Aritzia is aggressively investing into e-commerce and omni innovation, geographical expansion, product expansion, and brand awareness.

In this post I’m going to introduce you to the company, walk you through how they navigated COVID in such a way that benefited them, dive into their stellar earnings, and touch on what could propel their stock price higher in the future.

Let’s begin.

Company Introduction & Navigating COVID

Generally speaking, Aritzia is a design house that creates fashion brands who encompass “Everyday Luxury” for women. Think work-from-home apparel that you would also feel comfortable wearing out and about — with a little bit a flare.

For us non-fashion forward folks, the term “Everyday Luxury” might be hard to wrap our heads around. Lucky for us, Aritzia made this awesome graphic illustrating exactly where they lie within this ever evolving market.

Here’s a description of the company straight from the horse’s mouth:

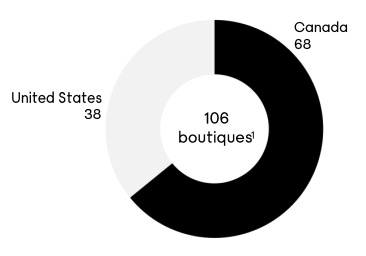

Aritzia is a vertically integrated design house with an innovative global platform. We are creators and purveyors of Everyday Luxury, home to an extensive portfolio of exclusive brands for every function and individual aesthetic. We’re about good design, quality materials and timeless style — all with the wellbeing of our people and planet in mind. Founded in 1984, in Vancouver, Canada, we pride ourselves on creating immersive, and highly personal shopping experiences at aritzia.com and in our 100+ boutiques throughout North America to everyone, everywhere.

As you can imagine, this company is pretty simple.

Unlike Asana, Upstart, or even Affirm — there’s not too much to wrap our heads around here. They’re a women’s clothing company selling “Everyday Luxury” items at scale throughout 106+ boutiques in North America.

These boutiques aren’t just your normal “come shop, check out, see you next time” environments. Aritzia takes pride in its boutique and concierge teams’ ability to deliver world-class experiences — resulting in loyal customer relationships.

For example, the storefront here in Nashville, Tennessee is incredibly inviting (first photo at the top). A recent reader of Rate of Return took a visit to a storefront near him with his wife while doing some “boots on the ground” research and here are his thoughts:

“I went to Aritzia in Mall of America. It’s next to Lulu. It was busy. Store design is awesome. A mix of organic wood and plants with classy bridal boutique dressing rooms. I spoke to sales manager and mentioned [the] stock. She was a transplant from Canada and was helping with the push into America. She verified the growth story and online presence.

They are poised for penetration. The store is designed to appeal to influencers taking photos. Her whole family owns [the] stock.”

The first boutique, however, was opened way back in 1984. It was a standalone boutique in Oakridge Centre — an upscale shopping mall in Vancouver, Canada.

Now, decades later, this standalone boutique has evolved into a massive design house with several brands operating underneath them. Each has its own vision, distinct aesthetic point of view, and a depth of design / quality that provides compelling value. All of the products sold within these “branded walls” feature high quality fabrics, considered detailing, and superior fit.

As you would imagine, their business is not just standalone boutiques. They’re also selling online through an incredibly immersive website — greeting you with examples and stories of what “Everyday Luxury” means to them.

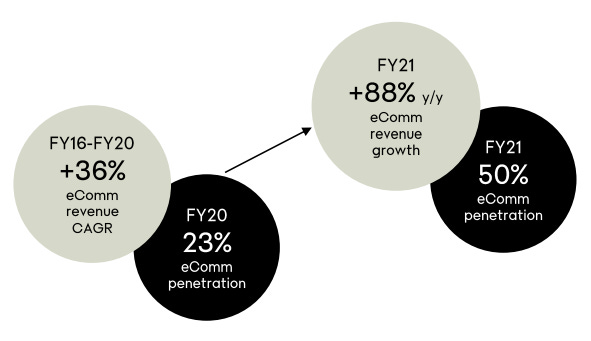

I have no clue what Aritzia’s website looked like from 2016 through 2020. However, whatever changes they made in 2021 worked. The company experienced a massive pop in e-commerce revenue growth, as well as penetration rate in relation to total revenue generated.

I’d argue the company’s ability to properly navigate COVID and the supply chain crisis that crippled thousands of businesses in 2020 and 2021 had a lot to do with it. I spent ~30 minutes or so listening to this presentation shared by the company’s CEO at a non-deal roadshow during mid-2021. Here’s my big takeaways so you don’t have to:

-

Work From Home: Aritzia immediately recognized the “stay at home / work from home” trend and shifted their product catalogue accordingly — leading to success.

-

Double Shoppers: They realized customers who shopped both in store and online were spending ~3X more annually — making this “convergence” a high priority growth strategy for the business.

-

Trendy Storefronts: Opening these new “trendy” stores around the USA is key to growth — they’re the #1 way Aritzia attracts new customers. Their e-commerce volume from folks that live around their stores increases +200%. This creates a flywheel that leans back into the previous bullet; an increasingly large group of customers is spending on average 3X more.

-

USA Penetration: During the pandemic, they rolled out across the USA — all of the stores they opened exceeded internal financial expectations. Driven by retailers closing their stores (Victoria Secret, etc.), allowing for Aritzia to snatch up favorable locations and start selling product.

-

To further explain this — the company has received countless inbound calls from historically great retailers with very favorable terms as these traditional retailers are forced to close shop. Again, storefronts are the main drivers to their e-commerce so this is only accelerating their flywheel.

-

Recent Earnings Results (4Q21)

You understand the business — let’s now walk through their most recent earnings release as well as their corresponding earnings call.

Reposting their wholistic results below so you don’t have to scroll:

-

Revenue: $453.3 million, an increase of +63% YoY

-

Gross Profit: $210.1 million, an increase of +67% YoY

-

Operating Income: $91.0 million, an increase of +89% YoY

-

Profits: $64.9 million, an increase of +113% YoY

Absolutely incredible. Their CEO, Brian Hill, spoke toward several big catalysts that drove these results on their call — USA penetration, e-commerce, as well as having all of their boutiques open for the first time since the pandemic started.

“In Q3, our business continued to surge, surpassing our own high expectations across all geographies and all channels. In the United States, we saw our business further advance at an unprecedented pace. In addition, our entire e-commerce channel sustained its exceptional momentum and retail in both countries flourished, with all boutiques open for the entire quarter for the first time since the start of the pandemic.”

“In the United States, our business has further accelerated at an unprecedented pace. Net revenue increased 115% from last year and 116% from 2 years ago, accounting for 44% of our revenue in the quarter. And of a particular note, we have almost doubled our active U.S. client base over the past trailing 12 months.”

However, the company was obviously impacted by supply chain constraints — forcing them to be extremely agile to keep up with demand. Their COO, Jennifer Wong, credits her team’s ability to source materials from several different geographies, strategically manage inventory, and use expedited freight when necessary.

“Thanks to our strong partnership with FedEx, we also achieved record service levels. E-commerce orders were expedited to clients, and we kept up with the unprecedented demand. All of these efforts kept us well positioned to sustain our sales momentum, especially heading into the holiday and will remain contributing factors as we continue to invest in delivering strong results going forward.”

Something awesome Jennifer shared is that during Black Friday and Cyber Monday they experienced record sales — not just in a single day, but in a single hour.

Finally, their CFO, Todd Ingledew, gave it to us straight.

“This exceptional performance is driven by the following:

First, we continue to see outstanding growth in the United States with net revenue in U.S. dollars of $159 million in the quarter, growing 126% or $88 million from last year and 128% or $89 million from 2 years ago. Our business in the United States comprised 44% of net revenue, up significantly from 33% in the third quarter last year. The sustained momentum in our U.S. business is reflective of the significant acceleration in our U.S. client base, which has nearly doubled in the last 12 months as more and more clients discover the Aritzia brand.

Second, our e-commerce business delivered another strong quarter with net revenue of $148 million, an increase of 47% on top of the 79% increase in the third quarter last year. The increased demand for our product manifested in both higher traffic and conversion during the quarter. E-commerce penetration was 33%, up significantly from 21% in the third quarter 2 years ago.

Third, retail revenue in the third quarter was $305 million, an increase of 72% or $128 million from last year and 45% or $94 million from 2 years ago. This remarkable growth was driven by both comparable sales and new and repositioned boutiques led by the strength in the United States. Retail comparable sales growth of 58% from last year and 26% from fiscal 2020 pre-pandemic was driven by both double-digit comp growth in Canada and the United States.”

This theme of “exceptional results” is carried into their guidance for not just the next reporting quarter, but the entire year of 2022.

“For the full year, we are increasing our outlook and now expect net revenue to be in the range of $1.425 billion to $1.45 billion, with the top end of the range up $150 million from our previous outlook. The updated outlook implies a full year revenue increase of approximately 65% to 70% from fiscal 2021.”

Finally, something incredibly important their CEO spoke toward during the Q&A section of the call was their pricing power and how they’ll leverage that to offset inflationary pressures.

“We’re hoping that the growth of our U.S. business will offset inflationary pressures of both the cost of goods that we’re selling and the labor or the logistics of getting our product there. We do expect more inflation to come along on both raw materials and labor and therefore, finished goods.”

As you could imagine, the positive affirmations Aritzia’s management team shared during this earnings call translated into positive analyst coverage.

Bank of America:

-

Reiterate “Buy” on Aritzia, as we think it’s one of the most consistent growers in retail with significant expansion opportunity in the USA

-

We are raising our full year 2022 & 2023 estimates to reflect momentum and increasing out price target to $62 CAD ($49 USD) to reflect higher estimates

The company offers outsized long-term earnings growth potential (we model a 20% 5-year CAGR) driven by square footage expansion and e-commerce growth.

Our $62 price objective is based on 41x our F2023 (C2022) EPS estimate, which is in-line with a set of growth peers. We think this valuation is warranted, given the company’s outsized growth potential in the US and online and its differentiated high-quality, full-price model.

Growth Drivers for the Future

Alright, Aritzia is a rockstar company with clear momentum — but what’s going to continue driving this company’s success throughout the coming years? Did you miss the boat?

The company is expediting investments across four strategic pillars:

1. E-commerce and Omnichannel Innovation

-

Enhancing digital experiences in efforts to reduce friction and drive conversion

-

Fit analytics, site optimization (improved shoppability), buy now pay later

-

-

Smooth omni-capabilities

-

View online and shop for it in store, buy online and pick up in store

-

-

Engaging services

-

Exceptional concierge services

-

2. Geographical Expansion

-

Open new boutiques in high traffic environments

-

Build brand awareness, significant client acquisition, fuel to e-commerce channel — new boutiques pay back within 12-24 months

-

-

2022 Expectations: +7-8 new boutiques (all in USA) and 6 boutique repositions (Canada & USA)

-

Identified 100+ locations in the USA that meet their criteria

3. Product Expansion

-

Goal is to double their total number of SKUs by the end of 2025

-

Depth (sizes, lengths, colors)

-

Breadth (new style development)

-

New categories (swim, lingerie, men’s)

-

-

Men’s is a big push for the company — acquired Reigning Champ, a leading designer and manufacturer of athletic wear

4. Brand Awareness and Customer Expansion

-

Begin leveraging digital marketing, social media, and influencer strategy

-

Launch a VIP program for their most loyal customers

Conclusion

There’s a ton of major developments happening for this company.

I’m excited to open a position and ride this “USA expansion” wave into 2025.

The company has an enterprise value of about $4.6 billion USD, which means they’re trading around ~21X forward adjusted EBITDA expectations. They’re also expected to print north of $230 million CAD in free cash flow, or about $182 million USD.

This translates to about $1.65 in FCF per share. With the average 35X multiple applied — we’re looking at ~$60 / share within the next 12-18 months.

This represents approx. +30% upside from current prices.

Wall Street’s 12-month average price target: $55 / share (USD)

Disclaimer: This is not financial advice or recommendation for any investment. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

BofA commentary from Alice Xiao and Lorraine Hutchinson, CFA.